Samsung and SK Hynix Rebound: A Bottom or Just Another Volatile Day?

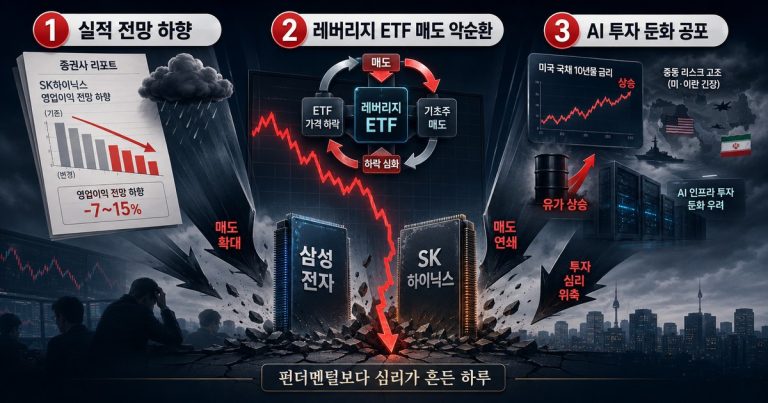

The Samsung and SK Hynix rebound arrived only one session after a historic semiconductor selloff. On July 14, 2026, Samsung Electronics closed 3.34% higher at KRW 263,000, while SK Hynix gained 3.69% to KRW 1,913,000. The KOSPI finished at 6,856.83, up 0.73%, after swinging between deep losses and gains during the session. The recovery did not erase the previous day’s damage, but it showed that large investors were willing to buy when fear pushed valuations sharply lower. The important question is whether this was the beginning of price stabilization or simply another violent move inside an unfinished correction.

What the market actually did

The closing index looked almost calm, but the intraday market was anything but calm. According to the July 14 market close report, individual investors sold roughly KRW 5.5 trillion of shares. Institutions bought about KRW 3.9 trillion, and foreign investors purchased approximately KRW 1.7 trillion. Most sectors declined, yet electrical and electronics stocks rose 2.76%. That combination matters more than the modest index gain because it shows where fresh risk capital was concentrated.

Samsung and SK Hynix were the main beneficiaries. The two stocks had fallen 10.70% and 15.37%, respectively, in the previous session. SK Hynix then traded as low as the KRW 1.67 million area on July 14 before recovering to close above KRW 1.91 million. The individual stock report illustrates how quickly forced selling, bargain hunting and short-term repositioning collided. The Samsung and SK Hynix rebound therefore signals renewed price discovery, but one positive close is not enough to prove that a durable bottom is in place.

Did institutional flows signal a bottom?

Foreign and institutional buying is constructive because these investors absorbed part of the supply released by frightened retail holders. It also suggests that some professional investors judged the reward-to-risk ratio to be better after the crash. However, daily flow data should not be treated as a perfect statement of long-term conviction. Program trading, futures hedges, index rebalancing and leveraged-product adjustments can all affect the numbers.

A more reliable bottoming process would contain several features. Selling volume should decline when the market retests its lows. Foreign and institutional purchases should continue for more than one session. Closing prices should stop finishing near the intraday low, and the feedback loop created by leveraged single-stock products should weaken. The Samsung and SK Hynix rebound needs this broader confirmation. If those conditions develop together, the rebound would carry more information than a one-day relief rally. If buying disappears as soon as prices rise, the market may still need another round of position clearing.

Why earnings previews will keep moving the stock

SK Hynix has not yet released its official second-quarter results, so brokerage previews will continue to produce different answers. Korea Investment & Securities estimated second-quarter revenue of KRW 80.9 trillion and operating profit of KRW 60.4 trillion in a July 13 report. That operating-profit estimate was about 8% below the prevailing market consensus near KRW 65 trillion and became one of the catalysts for the selloff.

On July 14, Mirae Asset Securities lowered its operating-profit forecast from KRW 70.7 trillion to KRW 62.3 trillion. Even after the reduction, it maintained a buy rating and argued that the share-price correction had already reflected much of the concern. The two current estimates are relatively close, but the old and revised forecasts show how widely assumptions can move. DRAM and NAND average selling prices, the HBM product mix, long-term supply contracts, production yields and exchange rates can change a quarterly model by trillions of won.

By contrast, a UBS preview reviewed by the author placed second-quarter operating profit more than KRW 10 trillion above Korea Investment’s KRW 60.4 trillion estimate. Public coverage of UBS’s broader view also shows a higher price target and a constructive assessment of long-term supply agreements and HBM4 shipments.

Investors should therefore avoid turning one preview into a final verdict on the company. Before the official late-July release, each new estimate may trigger sharp gains or losses. For the Samsung and SK Hynix rebound to last, revisions must stabilize. The useful questions are whether revisions are spreading across the analyst community, which operating assumptions changed, and whether the next-quarter outlook is being reduced as well. The official operating margin, HBM shipment commentary and forward customer demand will be more important than winning a daily contest between preview numbers. See the public coverage of UBS’s SK Hynix outlook for additional context.

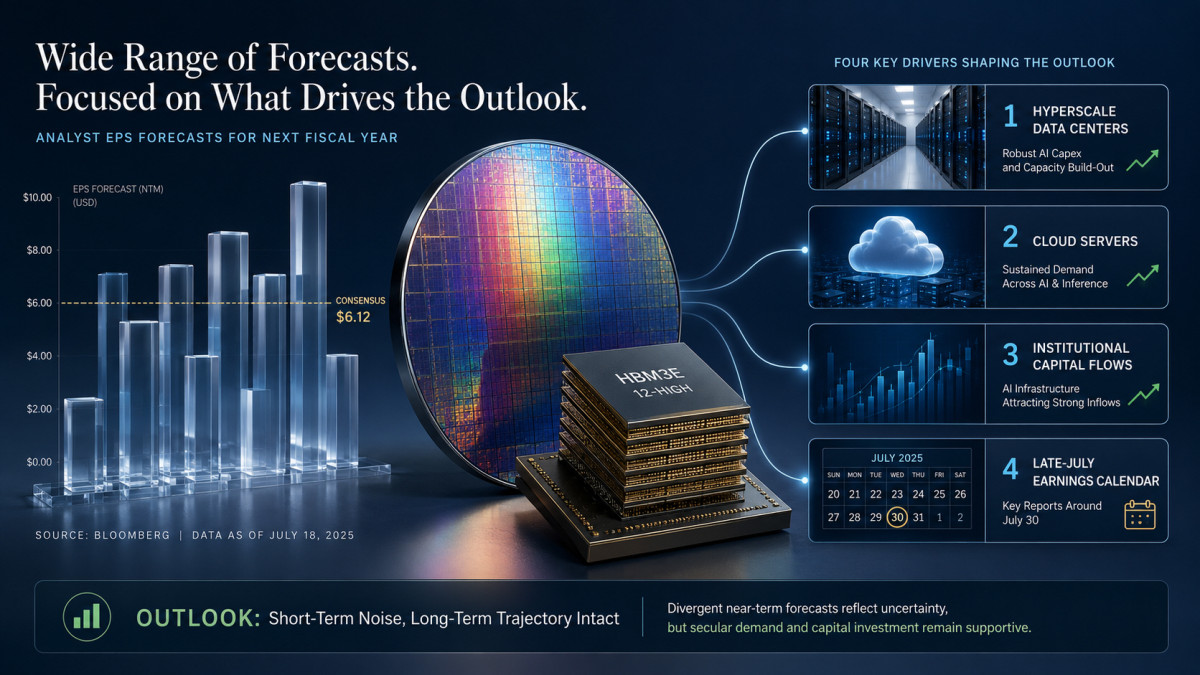

AI infrastructure spending remains the fundamental test

The medium-term earnings power of both Korean memory leaders depends heavily on hyperscaler AI infrastructure spending. Microsoft said in its latest earnings discussion that it expects roughly $190 billion of capital expenditure in calendar 2026. The company also said demand for Azure and AI capacity continues to exceed available supply. That is supportive for servers, networking equipment, power systems, HBM, high-capacity DRAM and enterprise SSDs.

SK Hynix’s official first-quarter results provide another reference point. The company reported operating profit of KRW 37.6103 trillion and an operating margin of 72%, attributing its performance partly to expanding AI infrastructure investment and increased sales of premium memory products. Those figures do not guarantee the second quarter, but they show that the underlying earnings base was exceptionally strong before the recent stock-market shock.

The bullish thesis would weaken if hyperscalers reduce capex guidance, delay data-center construction or indicate that AI monetization is not supporting additional investment. Investors should listen for changes in cloud growth, order backlogs, capacity constraints and component procurement during the late-July earnings season. Total capex is useful, but the composition and timing of spending are just as important for memory suppliers.

When staged buying makes sense

If AI infrastructure spending remains intact and official memory demand data stays healthy, a correction of 20% to 30% or more can create a more attractive entry range for long-term investors. That does not mean the exact bottom can be identified. A staged or dollar-cost-averaging approach is useful precisely because the path is uncertain. It spreads timing risk instead of assuming that one dramatic red day or one green rebound provides perfect information.

A disciplined plan should define the total position size, the number of purchases and the evidence that would invalidate the thesis. Investors can monitor five conditions: official SK Hynix results and HBM commentary; stabilization in analyst earnings revisions; continued foreign and institutional buying; unchanged hyperscaler capex plans; and a reduction in leveraged-product flow pressure. Those checks place the Samsung and SK Hynix rebound in a measurable framework. Purchases can be distributed across time and around major earnings events rather than concentrated before a binary announcement.

Risk control remains essential. Even a company with strong earnings can fall when expectations are too high, liquidity disappears or macro rates rise. The previous session’s structure is discussed in the related Samsung and SK Hynix selloff analysis. Reading the selloff and rebound together makes the central point clearer: fundamentals and flows can move in different directions for several sessions.

Conclusion: a useful signal, not final confirmation

The Samsung and SK Hynix rebound is meaningful because institutions and foreign investors bought aggressively after fear-driven liquidation. Current hyperscaler spending plans and SK Hynix’s official first-quarter performance also make it difficult to argue that the AI memory foundation disappeared overnight. At the same time, second-quarter operating-profit forecasts remain sensitive to assumptions, and the market is likely to react to every preview until official results arrive.

The rational interpretation is neither blind optimism nor automatic rejection of the rebound. Investors can treat lower prices as a possible staged-buying opportunity while requiring confirmation from earnings, AI capex and sustained flow data. The Samsung and SK Hynix rebound becomes a durable trend only if those three signals begin pointing in the same direction.

Sources

This analysis also references the Korea Investment earnings-preview coverage, the Mirae Asset forecast report, and Microsoft’s FY2026 third-quarter earnings discussion.

This article is for informational purposes only and does not constitute investment advice. Investment decisions and their consequences remain the responsibility of the investor. Verify the latest disclosures and market information before making any investment decision.