Hanmi Semiconductor Stock: Korea’s TC Bonder Leader Behind the HBM Boom

Hanmi Semiconductor stock gives foreign investors a direct way to understand the specialized equipment behind HBM production, AI memory, and next-generation semiconductor packaging.

Understand HBMRead Investment ThesisKOSPI-listed Korean stock

Precision die-stacking equipment

HBM and advanced packaging

Semiconductor capex exposure

Why Foreign Investors Should Know Hanmi Semiconductor

Hanmi does not manufacture GPUs, memory chips, or AI servers. It manufactures the equipment used to bond, inspect, and package the semiconductor components inside those systems.

Nvidia, SK Hynix, Samsung Electronics, Micron, and TSMC cannot expand advanced-chip production through chip design alone. They also require precise equipment capable of stacking memory dies, controlling heat and pressure, and maintaining high manufacturing yield.

Hanmi’s best-known AI-related product is the thermal compression bonder, commonly called a TC bonder. The company reported, citing TechInsights, that it held a 71.2% share of the global TC bonder market. That figure should be understood as company-reported.

What Is HBM?

HBM stands for High Bandwidth Memory. It is advanced DRAM designed to move enormous amounts of data between memory and AI processors at very high speed.

Higher Bandwidth

HBM transfers far more data than conventional memory architectures.

Better Efficiency

It reduces power consumed per unit of transferred data.

Compact Footprint

Vertically stacked dies sit closer to high-performance processors.

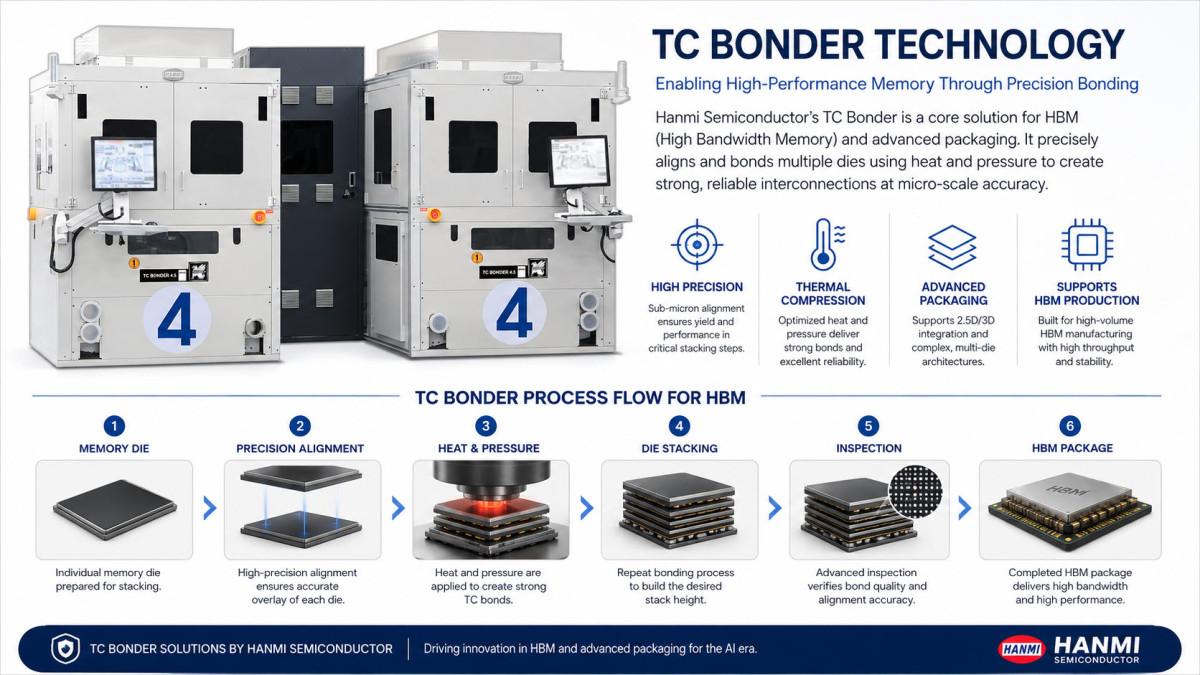

Stacking memory dies is difficult. Each layer must be aligned precisely, bonded reliably, and protected against heat-related defects. That is where TC bonders become essential.

What Does a TC Bonder Do?

A thermal compression bonder applies precisely controlled heat and pressure to align and bond multiple semiconductor dies.

The equipment must place each memory die with extremely high accuracy, create reliable electrical connections, and control heat without damaging the stacked structure.

The challenge becomes greater as memory manufacturers move from 8-layer products to 12-layer, 16-layer, and potentially higher stacks.

A Simple Analogy

Producing advanced HBM is like building a skyscraper with floors thinner than paper. Hanmi supplies the equipment that attempts to place each floor precisely, repeatedly, and at industrial speed.

What Does Hanmi Semiconductor Sell?

HBM TC Bonders

Equipment that stacks memory dies using controlled heat, pressure, and alignment.

Six-Side Inspection

Inspection systems intended to identify defects before and after stacking.

Micro Saw & Vision Placement

Systems for cutting, cleaning, visual inspection, sorting, and placement.

EMI Shielding Equipment

Equipment used to reduce electromagnetic interference in advanced packages.

Conversion Kits & Parts

Recurring revenue opportunities from upgrades and replacement components.

Next-Generation Bonders

Wide-die, hybrid, flip-chip, die, and 2.5D packaging bonders.

2025 Financial Performance

| Metric | 2025 Result | Investor Interpretation |

|---|---|---|

| Revenue | KRW 576.7 billion | Record annual revenue |

| Operating Profit | KRW 251.4 billion | Exceptionally strong profitability |

| Operating Margin | 43.6% | High-value product mix |

| Net Income | KRW 214.0 billion | Strong earnings conversion |

| Export Revenue | KRW 465.3 billion | About 81% of total revenue |

| Debt Ratio | 17.8% | Relatively conservative balance sheet |

Hanmi remained highly profitable in 2025, but investors should not assume that a 43.6% operating margin can be sustained through every semiconductor cycle.

Why Hanmi Has Built a Defensible Position

Customer Qualification

Equipment must pass extensive testing before entering mass production.

Vertical Integration

Hanmi says it controls casting, design, production, assembly, inspection, and testing.

Global Customer Experience

The company discloses relationships across memory, OSAT, and semiconductor suppliers.

Export-Oriented Revenue

Approximately 81% of 2025 revenue came from exports.

R&D Capacity

Hanmi states that roughly 30% of its workforce is involved in R&D.

Installed-Base Economics

Conversion kits, parts, and upgrades can create post-sale revenue.

The Core Case for Hanmi Semiconductor Stock

HBM Capacity Expansion

More HBM capacity requires additional bonding, inspection, packaging, and testing equipment.

Higher Stack Complexity

More layers and tighter tolerances increase the value of advanced bonding tools.

HBM4 Upgrade Cycle

New generations may require new machines, tooling, and inspection systems.

Beyond Traditional HBM

Hanmi is targeting 2.5D, chip-to-wafer, wide-die, and hybrid bonding.

New Manufacturing Capacity

The seventh factory is intended to support premium HBM and hybrid-bonder output.

Picks-and-Shovels Exposure

Investors are betting on equipment spending across the AI memory industry.

Samsung Electronics: Potential Upside, Not Confirmed Revenue

Samsung Electronics is an obvious potential customer because it is one of the world’s largest memory manufacturers and continues investing in HBM and advanced packaging.

However, Hanmi has not publicly disclosed a confirmed TC bonder supply agreement with Samsung Electronics. Samsung should therefore be treated as strategic upside rather than part of the base-case revenue forecast.

- Samsung needs HBM and advanced-packaging equipment.

- Hanmi has potentially relevant technology.

- A commercial relationship is possible.

- No TC-bonder contract should be assumed without official disclosure.

TSMC and the 2.5D Packaging Market

Hanmi has introduced bonding equipment that it says can be applied to packaging structures such as TSMC’s CoWoS. This does not mean that TSMC has placed a confirmed order.

Direct Foundry Orders

Hanmi could eventually qualify equipment directly with a foundry or integrated manufacturer.

OSAT Ecosystem Orders

The company could sell to packaging partners participating in advanced-packaging supply chains.

Addressable Market Expansion

2.5D and hybrid bonding could move Hanmi beyond conventional HBM die stacking.

Bull, Base, and Bear Case

Bull Case

HBM spending stays strong, Hanmi protects TC-bonder leadership, next-generation tools qualify, and new customers expand the market.

Base Case

HBM spending continues unevenly. Hanmi remains profitable, but revenue fluctuates with order timing.

Bear Case

Memory capex slows, competing technologies gain adoption, and new factory capacity is underused.

Key Risks Investors Should Understand

Equipment demand can fall when memory manufacturers delay investment.

The investment story is increasingly tied to HBM expansion.

Hybrid bonding or alternative processes could change the market.

Technical compatibility does not guarantee mass-production orders.

Rivals may improve performance, lower prices, or gain qualification.

A small number of large orders can drive annual results.

New capacity could be underused if demand is slower than expected.

Export-heavy revenue creates FX and geopolitical exposure.

A good company can still be a poor investment at an excessive price.

Frequently Asked Questions

Is Hanmi Semiconductor a chip manufacturer?

No. Hanmi manufactures semiconductor bonding, packaging, assembly, and inspection equipment.

What is Hanmi Semiconductor’s ticker?

Hanmi Semiconductor is listed on the Korea Exchange under ticker 042700.KS.

Why is Hanmi connected to Nvidia?

Nvidia AI accelerators use HBM. When memory suppliers expand HBM production, bonding-equipment companies may benefit.

Does Hanmi only sell to SK Hynix?

No. Hanmi discloses a broader customer list, but not every customer necessarily purchases HBM TC bonders.

Does Hanmi supply Samsung Electronics?

No confirmed TC-bonder agreement has been publicly disclosed. Samsung is potential upside, not confirmed revenue.

Does Hanmi supply TSMC?

No confirmed direct order has been publicly disclosed. Hanmi has developed equipment intended for 2.5D packaging categories used in CoWoS-related ecosystems.

Is Hanmi suitable for conservative investors?

Probably not as a low-volatility core holding. It is exposed to capex cycles, qualification risk, technology transitions, and elevated expectations.

A Picks-and-Shovels Supplier to AI Memory

Hanmi Semiconductor is one of the more strategically interesting Korean companies in the global AI supply chain.

Its story is not based on manufacturing AI chips. It is based on supplying precision equipment required to stack, bond, inspect, and package the memory used by those chips.

The Best One-Sentence Summary

Hanmi is not “the next Nvidia.” It is a specialized equipment supplier selling picks and shovels to the AI memory and advanced-packaging industries.

Official References

Visuals: the hero and TC bonder technology infographic were prepared for Korea Stock Insight. The TC bonder product image is used as a product reference for educational commentary.